Swedish buy now pay later giant Klarna enters NZ market

Swedish buy-now pay-later giant Klarna says it will aim to under-cut competitors as it enters the already crowded New Zealand market.

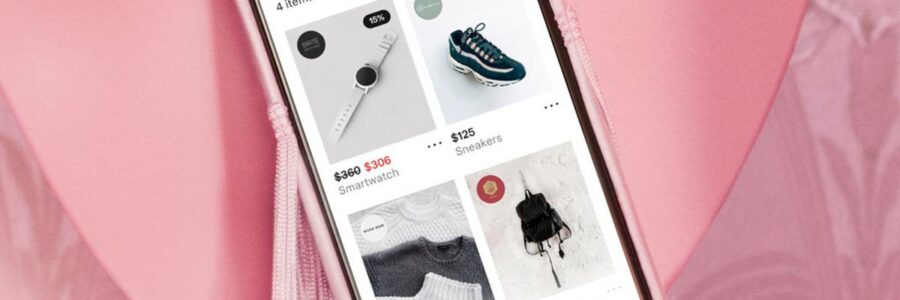

Klarna, which is in 21 countries worldwide, offers consumers the ability to pay off their purchase in four interest-free installments while getting the item upfront.

New Zealand already has a multitude of players which offer a similar service, including Australian firms Afterpay and Zip, as well as local BNPL provider Laybuy.

But Sebastian Siemiatkowski, Klarna’s CEO, says the company is not fazed by the number of rivals it faces to gain a foothold here.

“It is not the first time we have come into a crowded market. We have done that in the US – there were a couple of players already present when we came into the market.

“We do benefit from having global retailers, working with one provider, we have a couple of exclusive global partnerships.”

Klarna will leverage off its relationship with ASB bank, making it easy for ASB customers to sign up for the service while tapping into the bank’s business customers.

ASB’s parent company, Commonwealth Bank of Australia, owns 5 per cent of Klarna and the Swedish firm has already used that relationship to enter the Australian market.

Siemiatkowski says it is not only other BNPL players it sees as competitors but the credit card companies and PayPal.

But he says Klarna offers a service that is consumer focused, linking purchases to SKU data to allow people to easily track delivery of their purchases and what they have bought using images, making it easier to seek a refund or replacement.

“[If you] think about a credit card statement today – it’s fairly hard to understand, maybe it says the merchants name and amount. With Klarna you see images of the item you bought.”

/cloudfront-ap-southeast-2.images.arcpublishing.com/nzme/R33TGJULETESHXJP3WJ4AUJWGU.jpg)

Klarna offers consumers the ability to make wish lists of items they want to buy and then be notified when the price drops for that item.

It also gives the ability to buy product from merchants who are not signed up to the service through its app. For some other providers, merchants have to be signed up to use the service before a consumer can buy a product.

While consumers get an interest-free payment service provided they pay on time, merchants have to pay a percentage of the transaction to the BNPL provider.

New Zealand retailers have complained in the past about the hefty costs of using the services, which can sometimes clip up to 5 per cent of the cost of the item.

Siemiatkowski, who once described a competitor’s fees as extortionist, said the retail criticism was fair in some cases.

“That is why want to provide it at a more affordable cost.”

He said Klarna benefited from the fact it was not a start-up – it was founded in 2005 and already has more than 90 million consumers worldwide and has 250,000 retail partners.

“We can benefit from the fact we are a bank and have been live for 16 years. We have over a trillion dollars of revenue – we have a lot of the benefits of scale.”

So far it doesn’t have any local employees on the ground but Siemiatkowski said it hoped to employ two teams or up to 20 people in New Zealand to work for it.

“One of biggest strengths nowadays, what we try to do in all our locations, is build teams that support merchants.

“We have teams in China, Asia, every market in Europe, Canada, US and Australia. There is a lot of exchange of knowledge happening between those teams. So it’s crucial to put people on ground.”

The global pandemic has been good for online shopping and payments companies like Klarna.

While Siemiatkowski affirms this situation, he is also cognisant of the human toll of Covid-19.

“Definitely. But I want to say that with a big disclaimer because this obviously is a very tragic event that has impacted a lot of people. With that said, it is true in our case it has benefitted Klarna and it has had an accelerating effect on our growth because people have shifted more of their consumption to online and been buying more.

“We are seeing people shopping much more online. Spending overall has been down. But online has grown dramatically.”

In new markets it is younger shoppers, those in their 30s, who have taken strongly to the BNPL model, spurning credit cards in the process, but Siemiatkowski says in more established markets like Germany it has seen growth across the population.

“The younger demographic were already shopping more online. But in markets where we have all demographics shopping, the biggest increase in usage has come from those in their 50s and 60s.

“Their online consumption has increased massively.

“Obviously there is going to be a revival of the physical store. But I do believe we are not going to go the whole way back, we have found a new level.”

Source: Read Full Article